Value investing can protect against the corrosive effect of inflation

- Rob Davies

- May 31, 2022

- 2 min read

Updated: Dec 9, 2025

UK inflation figures came out this month with a print of +9.0%yy (April), from +7.0%yy (March) and slightly below +9.1%yy consensus estimate.

This is the highest level in 40 years and brings the UK’s cost-of-living crisis into sharp focus. Rising energy and food costs are the primary drivers, linked to the sanctions regime and the Russia/Ukraine war.

The Bank of England has been behind the curve regarding inflation risk. A look at inflation guidance contained in recent Monetary Policy Committee (MPC) minutes shows this. Near-term inflation guidance has consistently under-estimated inflation since August 2021 – rising from “above 2%”, to 4%, 6%, 8%, 9% and now 10%.

Although it may run counter to intuition in a volatile market environment such as we are seeing at present, equities are the ultimate long-term inflation hedge. Within equities, funds with a value/income bias help to ensure that valuations are based on the ability of a business to pass on inflationary costs and generate stable or growing earnings in excess of inflation. Income-yielding shares have an inherent value bias owing to the types of company that can pay a steady dividend: market value is underpinned by the twin fundamentals of near-term earnings and dividends. Because of this, Value equities tend to perform well in periods of inflation.

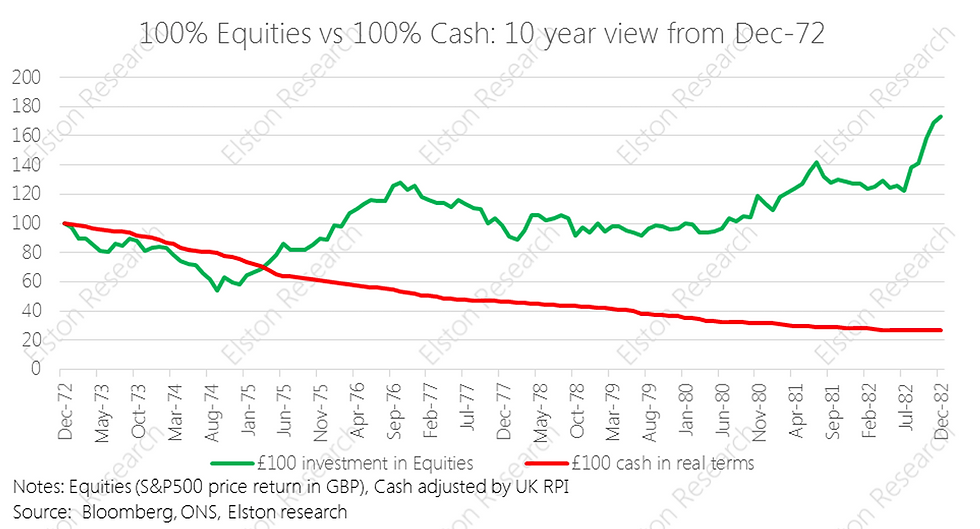

To understand the performance of asset classes during a high inflation regime, we can draw on lessons from the 1970s. To illustrate this, we show the performance of US equities (in GBP terms), relative to cash, during the 10 years from December 1972 - a peak inflationary regime.

On a 10-year view from December 1972, an allocation to equities delivered a price return of +72.9% (+5.6% annualised), ensuring capital growth in a high-inflation regime. Cash meanwhile lost -73% of its purchasing power (12.4% average annualised inflation).

When considering selection of equity income funds it is worth considering the strength not only of past dividend track record but forward-looking dividend growth too. Quality income funds exhibit persistency, whereby they pay a regular, stable and ideally increasing dividend over the long-term while at the same time endeavouring to mitigate concentration risk.

The emergence of inflationary pressure in the market is putting companies and funds with a value bias and a high-quality income stream back in the spotlight and deservedly so. UK inflation risk remains skewed to the upside and will run for at least as long as the Russia/Ukraine war, a situation that requires political, not economic, resolution.

For the longer-term, despite the inevitable anxiety fostered by short-term volatility, equities offer better inflation protection than cash in a high inflationary regime.

Comments